ROOTS OF THE 60/40 SPLIT

Modern portfolio theory examines how investors can construct a portfolio using different asset classes to optimize returns for a given level of market risk.1 First introduced by economist Harry Markowitz in the 1950s, modern portfolio theory remains a mainstay of the investing and finance world today.2

Under modern portfolio theory, the 60/40 allocation of 60% stocks (equities) and 40% bonds generally has represented a typical starting point for benchmarking risk tolerance.

As people age and get closer to retirement, this allocation often shifts, becoming more heavily weighted to bonds than stocks. Following modern portfolio theory, it would not be uncommon for a person nearing retirement to have a portfolio where the weighting of stocks and bonds is reversed: 60% bonds and 40% stocks.

Why stocks and bonds? Risk and reward are generally positively correlated in investments. The higher the risk of loss, the greater the potential for reward. The lower the potential for loss, the lower the potential for reward.

Combining stocks and bonds has generally been seen as a good way to balance risk and reward in a portfolio.

Stocks are both higher risk and higher reward. Bonds offer lower risk and lower reward. Additionally, bonds can provide a source of predictable income.

A NEW ASSET MIX?

Today, based on a variety of economic conditions, this mix of assets — stocks and bonds — is coming under increased scrutiny as an appropriate allocation for retirees.

First, bonds aren’t the only incomeproducing asset class that can be used to balance out the risks of stocks. Second, bonds are subject to certain economic factors, including inflation.

BOND BASICS

Bonds can help you add diversification and stability to your overall retirement strategy and are commonly considered less volatile than stocks. In fact, as interest rates have generally declined since the early 1980s, many bonds have provided solid long-term returns.

However, while bonds can be an attractive addition to an overall retirement income strategy, they are not without risk. In fact, if you’re counting on bonds to help you save for retirement or to generate retirement income, you could find that their value has decreased when it’s time for you to cash in or reinvest in another bond.

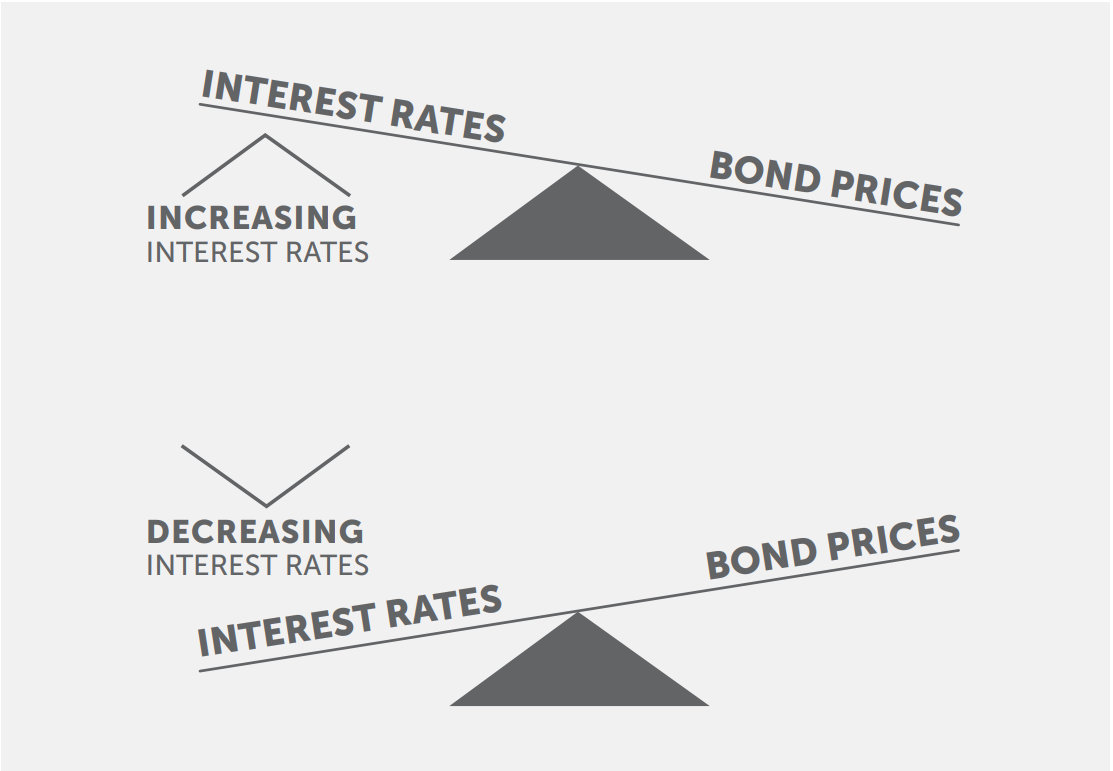

Bonds fluctuate in value in inverse correlation to changes in interest rates. When interest rates go up, a bond’s value goes down, and vice versa.

INFLATION’S IMPACTS

Current economic conditions — the highest interest rates since 2007³ and continued high inflation4 — may prove particularly troublesome for bonds. While interest rates are low, bonds seem like a good choice; however, as interest rates start to rise, bond values go down.

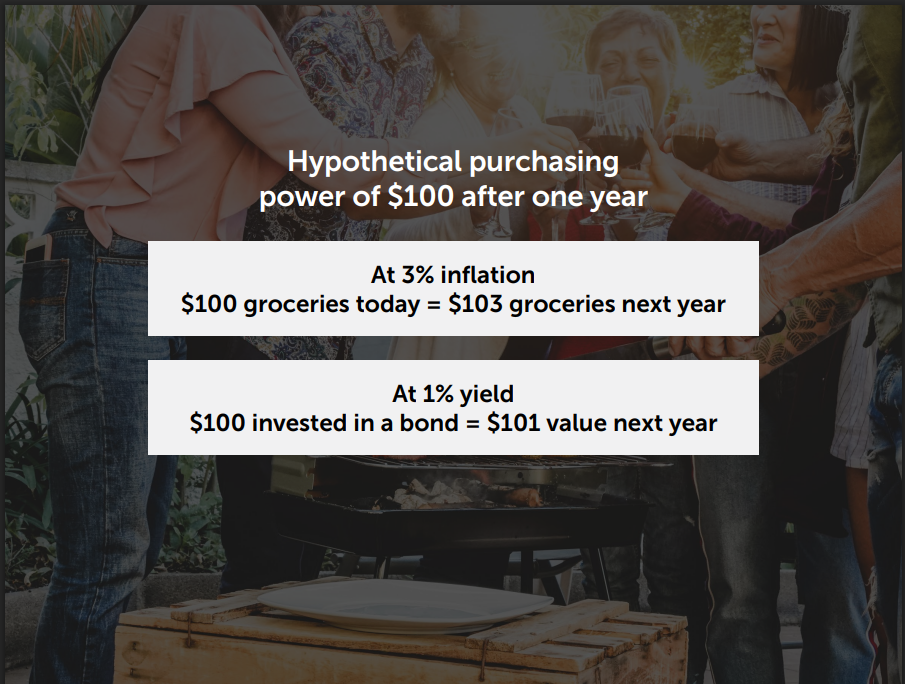

Meanwhile, inflation is responsible for pushing up the cost of the things we buy, and rising inflation lessens the purchasing power of one’s money, including any income derived from bonds. For example, consider a basket of goods that cost $100 at a grocery store today. If the inflation rate is 3%, that means that same basket of goods will cost $103 at the store one year later.5

Someone holding a short-term bond with a yield of 1% would see the value of a $100 bond investment rise to $101 over the year. But if the cost of goods is now $103, that person just lost $2 in purchasing power.6

While some inflation is a good thing that keeps the economy growing, the Federal Reserve tries to help achieve a balance so there’s neither too much nor too little, aiming for a steady 2% average inflation rate.7 One strategy the Federal Reserve uses to help control inflation is by influencing interest rates. When inflation is too high, the Federal Reserve typically raises interest rates.8 And as we’ve just discussed, those rising interest rates mean falling bond values. Longtime investor Warren Buffett has signaled his caution on bonds over the years.⁹ “

’Efficient’ markets exist only in textbooks,” Buffett said in his annual letter to Berkshire Hathaway shareholders. “In truth, marketable stocks and bonds are baffling, their behavior usually understandable only in retrospect.”¹⁰

ANOTHER INCOME OPTION

Bonds aren’t the only asset with less risk associated with market volatility and that can generate predictable income. Fixed index annuities are another option.

An annuity is a contract between you and an insurance company, where the purchaser pays a premium in exchange for a variety of guaranteed payout options for a set period of time or for the remainder of his or her life. The two phases of annuities are the accumulation phase, where the contract value accumulates interest earnings, and the distribution phase, where income is paid out from the annuity.

They are the only financial product that can guarantee income as long as you live. The guarantees of an annuity are backed by the financial strength and claims-paying ability of the issuing insurance company.

Fixed index annuities offer not only principal protection but also the potential to earn interest on your principal, up to a certain amount, based on an external market index such as the S&P 500. When you buy an FIA, you don’t own any shares of stock or participate directly in the market. You own an annuity contract.

FIAs credit interest to your annuity based on a formula (determined by the insurance company and outlined in your contract) that decides how additional interest from the index is calculated and credited to your contract value. FIAs offer protection of principal from market losses, along with the potential to provide higher interest than traditional fixed annuities.

There are several potential costs and limitations you should consider before purchasing an FIA.

- Your premium is not liquid, meaning you may not be able to withdraw it from the annuity without incurring surrender charges, which are penalties levied against withdrawals made before the surrender date stated in the annuity contract.

- You can purchase various optional riders with an annuity to offer additional benefits, such as enhancing your lifetime income in various ways, but those riders may come at additional cost.

- Caps establish how much of an index’s gains you participate in. For example, if an annuity has a cap of 3%, that is the maximum credited interest you can receive. If the index increases by 10%, you would receive 3%. However, negative returns in an index don’t negatively affect your annuity; if the index decreases by 3%, you receive no credited interest.

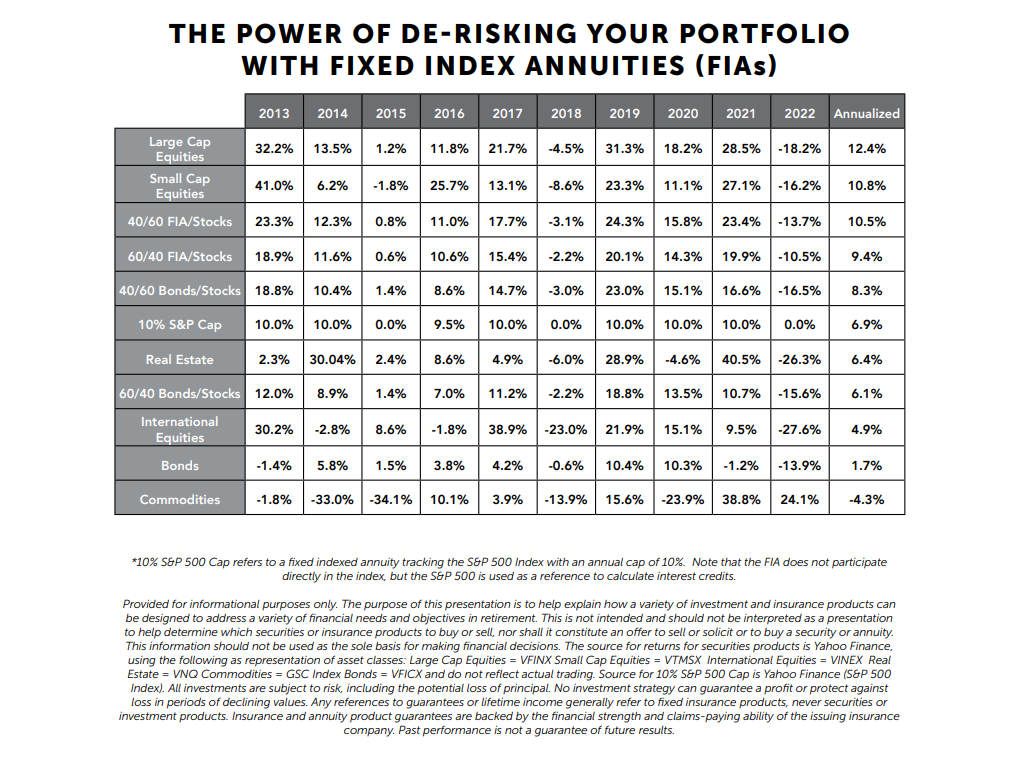

BALANCING RISK

This chart illustrates the hypothetical potential of using fixed index annuities (FIAs) as the financial tool to balance out the risk of stocks in a portfolio. Shown are the annual and 10-year average returns for some of the most common asset classes and portfolio mixes.

As you can see, timing the market is nearly impossible given that returns vary widely each year for almost all categories. This highlights the importance of having a diversified portfolio. If we look at simple diversification, combining two asset classes in a 60/40 “less risk, less potential/more risk, more potential” example, which is common for many retirees, we see that a 60/40 bond/stocks mix showed an average return of 7.89%. A 60/40 allocation featuring an FIA with crediting interest based on the performance of the S&P 500 Index with a 10% Cap (60%) and large cap stocks (40%) had an average return of 9.80%. This is just one example, using one type of annuity with a specific crediting strategy; it is provided not as a recommendation but as an illustration of the potential role an annuity can play in an overall retirement portfolio.

CONCLUSION

While stocks and bonds have been a traditional asset mix helping to manage risk, it’s worth considering whether a fixed index annuity could be another income-focused alternative to help balance risk. As you consider the risk and reward in your personal portfolio, know that there is no onesize-fits-all answer. That’s why it’s important to consult with a qualified financial professional who can assess your timeline to retirement and your level of risk tolerance before recommending a potential asset mix to help take you to and through retirement.

1 Kent Thune. The Balance. May 22, 2022. “What is Modern Portfolio Theory (MPT)?” https://www.thebalance.com/what-ismpt-2466539. Accessed March 8, 2023.

2 Ann Behan. Investopedia. May 5, 2022. “Harry Markowitz: Creator of Modern Portfolio Theory.” https://www.investopedia.com/terms/h/harrymarkowitz.asp. Accessed March 8, 2023.

3 FRED Economic Data. March 1, 2023. “Effective Federal Funds Rate.” https://fred.stlouisfed.org/series/FEDFUNDS. Accessed March 8, 2023.

4 Jeff Cox. CNBC. March 14, 2023. “Inflation gauge increased 0.4% in February, as expected and up 6% from a year ago.” https://www.cnbc.com/2023/03/14/cpi-inflationfebruary-2023-.html. Accessed March 14, 2023.

5,6 Thomas Kenny. Oct. 23, 2022. “The Impact of Inflation on Bonds.” https://www.thebalancemoney.com/the-impact-ofinflation-on-bonds-417071. Accessed March 8, 2023.

7 Ramsay Lewis. Business Insider. Oct. 13, 2022. “What is inflation? Why the cost of goods rise over time and what it means for the value of your money.” https://www.businessinsider.com/what-isinflation/. Accessed March 8, 2023.

8 Federal Reserve Bank of Cleveland. “Why Does the Fed Care About Inflation?” https://www.clevelandfed.org/en/our-research/center-for-inflation-research/inflation-101/why-does-the-fedcare-get-started.aspx. March 8, 2023.

9 Bram Berkowitz. The Motley Fool. March 4, 2023. “Stocks or Bonds? For Warren Buffett, It’s a No-Brainer.” https://www.fool.com/investing/2023/03/04/stocks-or-bonds-for-warrenbuffett-its-no-brainer/. Accessed March 8, 2023.

10 Jonathan Stempel. Reuters. Feb. 25, 2023. “Warren Buffett, in annual letter, stays upbeat and preaches patience.” https://www.reuters.com/business/warren-buffett-annual-letter-stays-upbeatpreaches-patience-2023-02-25/. Accessed March 8, 2023.

This content is provided for informational purposes only and is not intended to serve as the basis for financial decisions. The information and opinions contained herein provided by third parties have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed.

All investments are subject to risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Any references to guarantees or lifetime income generally refer to fixed insurance products, never securities or investment products. Insurance and annuity product guarantees are backed by the financial strength and claims-paying ability of the issuing insurance company.

Content prepared by Advisors Excel, with the assistance of Guaranty Income Life Insurance Company.

© Copyright 2023 Advisors Excel, LLC